Our Latest Blog Post's !

We spend so much money on bills and other costs of our daily lives that we feel like Superman when we think about how we have managed to keep everything together!

Your credit score is likely the most significant grade you’ll ever earn in life. It affects the credit cards and loans you may have, and the interest rates on your loans and mortgages you may have. If you want the finest financial opportunities, you must maintain the highest possible score.

It takes time to build a good credit history, but one bad decision may demolish it in a single day. AAR Financial is giving you 5 credit mistakes you should never make and tips on how to help you save your credit score from dropping.

1. Make Late payments

When you delay a payment to a debtor, two things usually happen; your lender reports the delinquency to credit bureaus, and you are charged a late payment fee.

You may also lose access to a promotion or offer, such as a reduced interest rate, in the future.

If you don’t want to pay late fees or interest and your poor repayment history is reported on your credit bureau, AAR Financial will help you by offering you guidance on how to avoid late payments.

Make a list of all your accounts, including mobile phone bills, utility bills, credit cards, loan payments, mortgage payments, and so on. Write beside all your accounts the due date every month, and outline this on a calendar on your fridge or your email calendar with a reminder. This way, you will always be on top of when your due dates are and never be late on a payment in the future and ensure there are funds in your account.

2. Use Your Full Available Credit on Your Credit Card

The total amount of money that may be charged to a credit card, including purchases, interest charges, and fees, is referred to as the credit limit. Every credit card has its own credit limit, which is determined by borrowers based on credit scores and other signs of eligibility. your credit limit is, crossing it is almost always a bad decision that most people make.

Below are the most common results of exceeding your credit limit:

It is possible that your credit card will be declined.

You may be charged an over-limit fee.

Your interest rates may increase.

Your credit limit may be decreased.

Your credit score may suffer as a result.

Using credit cards and not paying them off monthly can be detrimental to your credit.

3. Miss Payments

The repercussions of a missing payment could be hard on your credit score. We suggest that you make a list of all your debtors that you have accounted for and outline them on your calendar or on a note. We encourage that you pay at least the minimum due soon as possible.

4. Apply for Lots of Credit Cards

It’s not a good idea to apply for lots of credit cards at once as well as hold so many cards. The damage to your credit score is most likely one of your main concerns about having multiple credit cards. This is a negative overall, as your credit is taking a hit every time you apply for one. Not to mention, having many cards can become difficult to manage and remember their due dates.

What we suggest is starting with one credit card and getting used to managing that one card. Once you can manage this and understand how it can affect your credit score, then we suggest looking into more options if you should choose. If you have many credit cards, we suggest paying off the cards with the highest interest rate and closing those accounts so that you can focus on one or two cards that are more manageable.

5. Monitor Your Credit Score

People with bad credit never monitor their accounts, so even if they pay the whole amount on their credit card, their credit score tends to be low. Being fiscally responsible means always monitoring your credit score and your accounts to ensure you are on top of your payments. Always being on top of your finances also keeps your ahead and on top of fraud should it occur. There are many companies that provide credit monitoring services including TransUnion, Equifax, and Credit Karma.

Our children will play an important role in society and its activities one day, so it is important that we provide education on leading healthy financial lives.

We must provide as much support to our children in preparing them for tomorrow and ensuring that they are equipped to face any future financial challenges. One area where they require guidance is financial management as adults.

It’s difficult to talk about money, we get it. Talking about money with your children might be even more difficult! Should allowance be conditional on household tasks?

How do you keep your child from being spoiled? How do you handle college debt? Whether your children are 5 or 25, it is never too early—or too late—to encourage them to develop financial confidence and responsibility.

AAR Financial will educate you on how to raise financially responsible children and provide them with the education they need to make good decisions as they get older

1. Have an open conversation about finances.

Talking openly about money is an important element in supporting children in establishing a healthy relationship with money. “Talking about money should not be limited to a one-time chat,” says AAR Financial.

“It has to be part of your daily conversation.” When money issues arise and your children are there, discuss with them as freely and soon you will both feel more comfortable and at ease.”

Including your children in basic financial decisions is one method to do this. For example, before deciding what to prepare for dinner, you may go through the grocery list together and establish your budget, so you don’t spend outside of your budget.

You might also start a conversation about why certain items are more costly than others. Ask for help from your children in comparing prices at the grocery store and make a game out of it! Is the product almost the same but more expensive since it is a name brand? Or are there other benefits, such as a higher Item 1 or Item 2, that might justify a higher price?

2. Open a bank account for them.

Choose the bank that offers the most exciting savings account offers. Bring your children to the bank and explain the difference between a chequing account and a savings account.

Tell them that when they receive a large amount of money as a gift or for a birthday, they should deposit it in a savings account that you don’t use for a long time. If you need money to spend, transfer it out of your savings account into your chequing account. You can also explain to your children how the money from their piggy bank if they have one can also be put into the bank.

3. Take them shopping.

Take your children with you while you go shopping. Show them what they need to buy first and avoid perching on unnecessary products. Spend your money wisely. This is the most important aspect of growing their financial responsibility.

4. Encourage part-time work.

Allowing your children to work part-time is a fantastic lesson in training them to stand on their own feet and the value of money. The summer is a great starting point, especially since there is no school.

McDonald’s and Tim Horton’s are great places to start for children to strengthen their communication skills, learn how to interact with others as well as learn the value of money.

5. Motivate entrepreneurship.

Entrepreneurship turns children into leaders capable of leading independent and successful lives. Make sure your children understand the importance of entrepreneurship and that it is a choice for them so that they can create their own chances when the time comes.

Start small, with enjoyable activities like assisting them in running their own juice stall at home or cookie sale on your street, which will help kids develop stronger financial management skills, and encourage creativity.

Encourage collaboration while stressing the importance of goal setting and preparation. Teach children that failing is okay and that errors simply create additional opportunities to learn and discover new methods to achieve goals. We appreciate you reading our blog and hope it will be helpful in educating and raising financially responsible children!

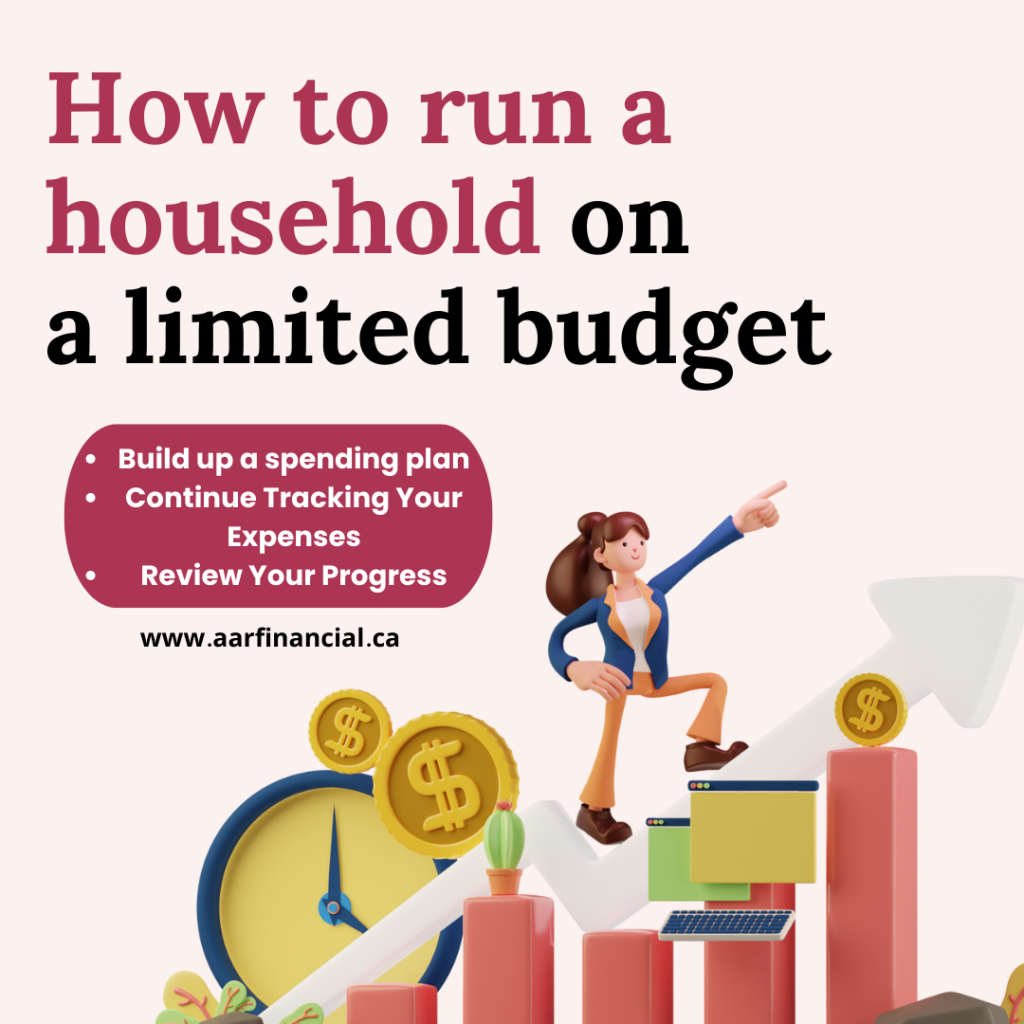

To manage your household budget, you simply need to be wise about your spending patterns, not necessarily brilliant at math!

Contrary to popular belief, keeping a household budget involves more than just getting by.

Additionally, a portion of your gross income should be set aside for an emergency fund and debt repayment (if you have any).

AAR Financial offers the most comprehensive guidance for handling household budgets.

1. Build up a spending plan.

Let’s start with groceries. When people go to buy groceries, they frequently purchase necessary items but also unnecessary items.

This is not entirely our fault, as multinational corporations have marketing tactics that convince us we NEED other items.

Avoid getting into this trap and stick to a grocery list, so that you don’t spend too much money. Start with making a list of your weekly spending and analyze it.

Only spend money on items that are necessary for your daily routine with you and your family.

Additionally, there are many flyers that are available online and are also sent out in the mail which you can usually use towards your weekly shop.

If you have a big family, do your homework, and make some comparisons between buying at a regular grocery store or buying in bulk from Costco.

It may be cheaper, but also note there is a yearly fee so ensure you take that into account.

Now, this can be applied to other facets of your life as well to stay on track and organized. A spending plan and a quick chart and list can assist you with other household expenses such as tv and internet, cell phones, hydro, etc.

Staying organized is the key to staying on track and excel is also a great tool for organizing your expenses.

Make it an activity to work on with your partner and spend an evening organizing your expenses so that you both are on the same page.

2. Continue tracking your expenses.

A cost tracker can help you with budget planning if you’ve tried other alternatives before and found they did not work for you.

Keeping track of your expenses doesn’t just mean keeping all your receipts or keeping a permanent record of every dollar you spend.

It’s a lot easier than that if you have a cost tracker or a list.

The difference between developing a budget that succeeds and one that fails is tracking costs.

Knowing where your money goes is the only thing that will ensure that your budget works, regardless of whether you are about to begin budgeting or have been doing so for years.

You may keep tabs on your expenditure using a variety of tools, such as apps, computerized Excel tracker spreadsheets, printed expense diaries, and journals.

It’s up to you how you want to keep track of your expenditures, but ensure you adopt the method that works best for you.

3. Review your progress.

You’ll feel different once you start living within your means and have some expense lists to refer to.

You’ll feel lighter, sleep better, and experience less financial stress from this organization.

Consider the differences between how you feel about managing your money today and how you felt when you first started.

Set up check-ins with yourself to see how your financial strategy is progressing. Consider the things that have and haven’t been operating well recently.

What changes can you make to make your life simpler?

Consider a few unforeseen costs that have occurred over the last several months. What did you do about those? Is there anything you could do differently to handle them better in the future?

Reviewing your development is a worthwhile experience when you have the time. Start by setting aside 10 minutes once a week, and over time you’ll be able to extend your check-ins to once per quarter.

Your wallet may suffer as we approach the holiday season. The spending doesn’t end with presents, though. Other costs associated with the holidays include those for eating, entertaining & much more.

When you add it all up, it’s easy to spend thousands of dollars on holiday happiness and begin the new year with crippling credit card debt.

AAR Financial has some holiday spending tips to help get you through the season with your wallet intact.

1. Make a Budget – Making a budget that covers all costs, from gift-giving to cooking a meal for all your family and friends, is the key to having a budget-friendly Christmas season.

2. List Expenses – Many people only aim for an approximate amount or estimate their expenditure based on recollection. Instead, make a few budgetary calculations based on your monthly outlays to come up with a more precise estimate for your holiday expenditures.

-> Gifts – Make a list of everyone you want to buy gifts for this year. Include all the tiny items you need to purchase for social gatherings, such as host and hostess gifts or a secret Santa gift exchange at work, in addition to the large gifts you need to buy for friends and family.

-> Mailings and cards – Include a line in your budget for the expense of purchasing or printing Christmas cards, photos, letters, calendars, and postage if you send them out.

-> Food – This area contains the food and beverages you’ll serve at your holiday parties, your family meal, and any potlucks you’ll be attending.

-> Decorations – Your list should have a line for any holiday decorations you intend to purchase. That includes things like a Christmas tree, any inside and outdoor lights that need to be replaced, and candles.

-> Clothing – Most of the time, you can wear clothes from your closet to dress for a holiday party. But you should also add anything specific you might need, like an ugly sweater for a theme party, if you don’t already have one.

-> Travel costs – Travel expenses are a huge additional expense that you must plan for if you are traveling for the holidays. Gas and tolls fall under this category if you drive. If you’re traveling, it also covers the price of your tickets, baggage fees, and any parking or shuttle expenses incurred at the airport.

3. Set Priorities – If your list of Christmas expenses seems a bit lengthy, don’t get alarmed. If there’s no way you can afford to pay for everything with the budget you have, you simply need to establish some priorities. As you go through your list, assign a number to each item based on its importance to you. Give your biggest priority the number “1,” your next-highest priority the number “2,” and so forth.

4. Shop Smart – If you are unable to reduce your gift list, purchase wisely to stretch your money. Think about purchasing some holiday gifts online. In addition to the convenience, it is simpler to compare costs and use discount codes. You’re also less likely to overspend because you’re avoiding the busy Christmas environment at the store.

5. Keep Track – Once you begin the holiday season, keep track of all your purchases. Bring your gift list, along with your budget sheet, with you on every shopping trip. Additionally, be sure to keep track of the cost of your holiday-related outings and other expenses so you will be able to more accurately budget next year.

There are also several tools to help you keep track of your spending within specific budget categories. One of the simplest is an old-fashioned envelope system, in which you create a physical envelope for each category – like gifts and decorations – and load it up with the appropriate amount of cash.

6. Look for more affordable alternatives – For most people, gift-giving isn’t the special thing about the holidays – it’s a unique holiday tradition that they share with their loved ones each year. Affordable holiday activities can help you create amazing memories such as: –

-> Watching a movie at home with some hot chocolate

-> Decorating the house together

-> Baking together as a family

-> Reading favorite holiday stories

-> Seeing a high school production, such as a play or choir performance

Once the holidays are over, recheck your budget and see how well you managed to stick to it. If you went over budget in some categories but stayed within your total spending limit, that’s a sign you need to tweak your budget next year, allocating more money to those categories.

As we begin a new year, we set new goals and make plans for the future. We have all experienced the frustration of increased prices at the grocery store and at the gas pumps after two hard years of surviving in a pandemic, many of us enduring layoffs at work.

Here are some suggestions to keep your finances on track in 2023.

A budget is a useful tool for planning costs and staying within one’s means of support. It establishes clear parameters for spending decisions and aids in bringing order to your finances.

When budget-based decisions are made often and consistently over time, they will result in increased savings without causing you to cut back on spending on the things you enjoy.

Looking for a good starting point? AAR Financial has some great budget-conscious tips and strategies.

1. Set Realistic Financial Goals: Setting short-term financial goals, as well as midterm and long-term, is an important step toward becoming financially secure.

We suggest taking the 50/30/20 budgeting approach. That means allocating

- 50% of your income toward needs,

- 30% toward wants and

- 20% toward savings and debt repayment.

By following the 50-20-30 rule, individuals have a plan for how they should manage their after-tax income. If they discover that they spend more than 20% of their income on wants, they can identify strategies to lower those costs so that money can be allocated to more crucial areas, such as retirement and emergency funds.

Although it is not advised to live like a Spartan, life should be enjoyed, having a plan and following it will enable you to pay for your expenditures and save for retirement, while also engaging in the activities that bring you joy.

2. Eliminate Bad Spending Habits:

Humans have a tendency to spend more money than we earn which will create problems in the future. It’s normal to follow your intuition and spend too much money. But it’s also crucial to maintain strict control over your costs.

For that, the first and foremost step is creating a budget. This means writing out your income and expenses and knowing exactly what you spend and where. All right, here are some areas which we need to focus on:-

- Know what you’re spending money on.

- Shop with a goal in mind.

- Think about big purchases.

- Do your grocery shopping online.

3. Be Disciplined: Discipline is the bridge between goals and accomplishment. Yes, maintaining your monthly budget objectives requires discipline.

However, only spending with control will enable your budget to pay off. You can establish weekly financial restrictions and regular reminders to better manage your spending.

Make a strategy, for instance, that your weekly expenditure won’t be more than 10% of your pay. Here are some of the best ways to achieve being more disciplined with your money:-

- Savings first – Save money first. You should save aside 10–20% of your salary for the future. Your retirement is the future, not next week or next year. If you receive a government pension, this is automatically done for you; otherwise, you are the only one who is making retirement savings.

- Set aside money for emergencies – Take $100/pay and set it aside in a savings account you don’t touch except for real emergencies. A real emergency is not dinner out or regular bills – it is losing your job, a roof collapsing, or someone in your family getting sick. It is important to be strict with yourself. If you cannot afford dinner out – don’t dine out.

4. Understand Your Spending Triggers: Finding the emotional and psychological factors that lead us to spend is frequently the key to learning how to quit spending. You’ll eliminate the temptation and opportunity to overspend if you take away those triggers.

• Environment: Craft fairs, shopping centers, home exhibits, and even holidays are good examples of situations where you’re more inclined to spend impulsively. These situations might either make you want to spend or make you feel forced to spend simply because you’re there. So, eliminate the temptation by either avoiding such settings or traveling with a small amount of money.

• Peer Pressure: Do you spend more money when you’re out with your friends than you normally would? If you can’t afford to eat, shop, or vacation like your friends, it’s okay to decline their invitations.

Instead, suggest plans that won’t cost you a lot of money. Meeting for coffee instead of brunch, exploring new hiking trails instead of going to the latest concert, or hosting a potluck dinner at home. You won’t be able to afford expensive vacations or fine dining, but you can still enjoy yourself.

Don’t be hesitant to tell your friends that you’re trying to save money; perhaps they’ll assist you on your journey, and some may even join you! What matters is that you surround yourself with friends who will encourage you as you work toward your financial objectives.

5. Keep a Track: To stay on budget, be sure you can track your plan, which is perhaps the most important step. Make certain that your expenses can be revisited at any time if necessary. We all have hectic schedules, and it can be difficult to remember every transaction detail.

Keeping a tracker can help you keep track of your expenses and analyze where your money is going the most. Tracking your expenses is essential for budgeting success because it holds you accountable for every dollar you spend. When you know where your money is going, you’ll be able to make better spending decisions and identify areas where you can cut back.

Budgeting is, in some ways, a state of mind that must be developed through constant practice. Focusing on what you want and knowing that small daily steps can help you get there can help you make budgeting a way of life.

For many people, the term “Debt Consolidation” might be confusing because of it’s variety of Debt management choices. However, today we’re exploring the subject of Debt Consolidation to clear up any confusion.

Debt Consolidation is a great strategy that combines outstanding, unsecured debts into one monthly payment. It often comes with a lower interest rate than what you were paying out while also giving your credit score a nice boost. Some effective ways to consolidate your debt include taking out a personal loan, a home equity loan, or even a 401 (k) loan.

AAR FINANCIAL specializes in debt consolidation solutions, offering the best credit counselling as well as personal loans and home equity loans. Find out more about the many debt consolidation alternatives you have by contacting one of our representatives at any one of our branches. If you need assistance with debt consolidation, we are pleased to go over your options in greater detail and assist you in making the right choice.

Let’s take a closer look at what debt consolidation can do for you.

How Debt Consolidation Works:

Debt consolidation is the process of combining multiple debts into one simple repayment loan. If you have multiple types of debt, you can apply for a loan to combine them into a single payment and pay them in one payment to keep your household and finances organized.

Finally, some people consolidate debt to simplify their bills by paying only one lender rather than multiple lenders. You can roll old debt into new debt in a variety of ways, including with a new personal loan, credit card, or home equity loan. Then you use the new loan to pay off your smaller loans.

Some Key Takeaways:

- Debt consolidation is the act of taking out a single loan to pay off multiple debts.

- You can use a secured or unsecured loan for debt consolidation.

- New loans can include debt consolidation loans, lower-interest credit cards, and home equity loans.

- Benefits of debt consolidation include a potentially lower interest rate and manageable monthly payment.

Strategies for Consolidating Debt:

You can consolidate debt by using different types of loans. The type of debt consolidation that will be best for you will depend on your current loans and financial situation.

There are two broad types of debt consolidation loans: secured and unsecured loans. Secured loans are backed by an asset like your house, which works as collateral for the loan. Unsecured loans, on the other hand, are not backed by assets and can be more difficult to get. With either type of loan, interest rates are still typically lower than the rates charged on credit cards. And in most cases, the rates are fixed, so they do not vary over the repayment period.

Here are some common ways to consolidate debt.

Personal Loan:

A personal loan is an unsecured loan from a bank or credit union that provides a lump sum payment to use for any purpose. What’s great about these loans is that they often offer flexible terms (typically 12 to 72 months) and establish a consistent month-to-month payment due, which assists in budgeting. As a bonus, financial institutions will make a payment directly to the creditors, saving you the hassle.

Home Equity Loan:

If you are a homeowner who has equity, a home equity loan or home equity line of credit (HELOC) can be a useful way to consolidate debt. These secured loans use your equity as collateral. Since there is an underlying asset for these loans, the rate is often lower than what you would get with a personal loan, making either the monthly payments smaller or avoiding higher interest rates from other lenders. The lower interest rate may give you the ability to pay down the balance more quickly. There could be additional mortgage-related expenses when taking this route, so a direct inquiry with your lender is a must.

Making Debt Consolidation Work for You:

Debt consolidation can be a good way to pay off high-interest debt while also saving money. However, it is not for everyone. Before taking out a debt consolidation loan, make sure you understand exactly what you’re getting into. Consolidating your debt is just the beginning of a long process. Here are key components to making it work.

- Make a realistic budget.

- Compare consolidation products and enable support for your goal.

- Shop around for the lowest interest rate.

- Read all the fine print and understand what will happen if you fail to make a payment or default on your loan.

- Pay more than the minimum payment.

- Make sure you are aware of any fees.

Debt Consolidation and Credit Scores:

Your credit may be impacted by several lenders if you are not able to keep up with your payments to them. Debt consolidation can be a useful strategy for paying down debt more quickly and reducing your overall costs in interest. You can consolidate debt in many ways, such as through a personal loan, new credit card, or home equity loan. Consider consulting with a professional financial advisor or with a reliable adult or friend for guidance on the options that may best fit your personal situation. There is one thing you can do to improve your credit score over time i.e., improve your payment history.

The bottom line:

There is no one-size-fits-all solution to debt management. As previously stated, debt consolidation can be a useful strategy for paying off debt more quickly in a variety of ways, such as with a personal loan, a new credit card, or a home equity loan. Before you take the advice of a single creditor, consider all your options so that you can make an informed decision. There are debt consolidation options as well as payment consolidation options. Some options require you to borrow more money, while others require you to restructure your budget.

Some options have a greater impact on your credit rating than others, and there are even options with interest relief to help you get back on track. “The right option will help you improve your money skills and provide you and your family with a financially stable future”.

Saving money is kind of like eating a healthy diet.

You know you should do more of it, but it’s hard to resist making spur-of-the-moment choices that make you happier now but worse off later. A tax refund marks a great chance to set yourself in a better position for the future. As tax season approaches, many people begin to anticipate receiving their tax return. For some, it may be a small windfall, while for others, it may represent a significant amount of money.

Word to the wise: Don’t wait until tax time to educate yourself.

Childcare expenses and family benefits:

You need to file your taxes every year to continue receiving family benefits like the GST/HST Credit and the Canada Child Benefit (CCB). If you’re a family with a low to a modest income, the GST/HST credit can offset a portion or all the sales tax you pay, including the tax paid on a new or used car.

The CCB is a tax-free monthly payment that helps cover the costs of raising children under the age of 18. It currently offers up to $569 per month for each child under age 6 and up to $480 per month for each child between the ages of 6 to 17.

Registered Retirement Savings Plan (RRSP) contributions:

Contributing to your RRSP is an excellent way to lower your tax bill and get a larger tax return. Your contribution limit is 18% of your earned income from the last tax year, plus any unused amounts from previous years. You can find your contribution limit in your CRA My Account or on your last notice of assessment.

A good rule of thumb is to maximize your RRSP if you make over $50,000, so you can benefit from the highest amount of tax savings.

Interest paid on student loans:

If you or your child is studying at a post-secondary institution, you can deduct the interest paid on a student loan if you received the loan under the Canada Student Loans Act, Canada Student Financial Assistance Act, Apprentice Loans Act, or similar laws in your province or territory. This deduction does not apply to something like a personal loan or line of credit. Apply this deduction if you owe taxes. Otherwise, it’s better to carry it forward.

Your student loan interest claim is a non-refundable tax credit. It can only be used to lower your tax bill and cannot be used to receive a tax refund. Since you can carry forward student loan interest for up to five years, it might be wise to save your claim for a year when you owe a lot of tax.

Medical expenses:

The CRA permits you to deduct a range of medical expenses as non-refundable tax credits, including the cost of orthopaedic shoes, laser eye surgery, dental cleanings, and private insurance premiums.

Union/professional dues:

Most professional association fees and union fees can reduce your taxable income. Examples of eligible expenses include trade union membership fees, professional board dues required under provincial or territorial law, and insurance premiums related to your profession.

Vehicle expenses:

You might be eligible to deduct some vehicle costs if you use your car for work. You could be able to deduct vehicle-related costs like gas, insurance, license and registration fees, maintenance and repairs, leasing charges, and interest on loans used to buy a car if you’re self-employed.

Depending on whether you lease or buy your car, there are various deductions. Capital cost allowance (CCA), a deduction used over a number of years based on the depreciation percentage, is available if you purchase (until the car gets old and has no more value). The amount of CCA you can claim for business use is capped at certain vehicle prices.

Under certain conditions, salaried employees may also be eligible for automobile expenditure deductions. The complete eligibility requirements are available here. Remember that travel time between your home and place of employment is not deductible.

Here are some smart financial moves you can make to get the most out of your tax return.

Pay off high-interest debt.

Using your tax return to pay off high-interest debt, such as credit card debt or personal loans, might be a wise financial decision. You can save a lot of money in interest payments over time and free up your finances to concentrate on other financial goals by paying off this debt with your tax return.

Build an emergency fund.

Now is a perfect moment to build an emergency fund if you don’t already have one. A safety net called an emergency fund can assist you in paying for unforeseen costs like car repairs, medical bills, or lost income. A wise financial decision that can provide you peace of mind and prevent you from getting on debt in the event of an unforeseen need is using your tax refund to kickstart your emergency fund.

Make a large purchase or investment.

In conclusion, using the information on your tax return might help you make the most of your financial condition. Think about utilizing money to make a significant purchase or investment, pay off debt, create an emergency fund, invest in your retirement, or donate to a good cause.

Debt Management: Tips to pay Your Loan on Time

Taking out a loan can be a great way to achieve your goals and fund your dreams.

However, with any loan comes the responsibility of repaying the borrowed amount on time. Repaying your loan on time is essential for maintaining a good credit score and avoiding late fees and penalties.

AAR Financial giving you some tips for managing debt and repaying your loan on time.

Set up a Budget:

The first step towards managing your debt is to create a budget. Start by reviewing your monthly expenses and income and determine how much you can afford to put towards your loan repayment each month.

By having a clear understanding of your budget, you can plan and make sure that you’re not taking on too much debt. It’s essential to prioritize your loan repayment in your budget and ensure that you have enough money to cover your payments each month.

Prioritize your Payments:

If you have multiple loans or debts, it’s important to prioritize your payments based on interest rates and the amount owed. Focus on paying off high-interest debts first, as they can accumulate quickly and become difficult to manage.

Make sure to also meet your minimum monthly payments on all your loans to avoid late fees and penalties. Prioritizing your payments can help you manage your debt more effectively and reduce your overall interest payments.

Create a Monthly Bill Payment Calendar

Use a bill payment calendar to help you figure out which bills to pay with which paycheck. On your calendar, write each bill’s payment amount next to the due date. Then, fill in the date of each paycheck.

For Instance, If you get paid on the same days every month—the 1st and 15th—you can use the same calendar from month to month. But, if your paychecks fall on different days of the month, you’ll need to create a calendar every month.

Consider Automatic Payments:

Setting up automatic payments is a great way to ensure that you don’t miss a payment. This can help you avoid late fees and protect your credit score.

Many lenders offer this option, so be sure to check with your loan provider to see if it’s available. Automatic payments can help you manage your debt more effectively and ensure that you don’t fall behind on your loan repayment.

Build an Emergency Fund to Fall Back On

Without access to savings, you’d have to go into debt to cover an emergency expense. Even a small emergency fund will cover little expenses that come up every once in a while.

First, work toward creating a small emergency fund—$1,000 is a good place to start. Once you have that, make it your goal to create a bigger fund, like $2,000. Eventually, you want to build up a reserve of three to six months of living expenses.

Make Extra Payments:

If you have some extra cash, consider making additional payments towards your loan. This can help you reduce your overall interest payments and pay off your loan faster.

Make sure to check with your lender to see if there are any prepayment penalties before making extra payments. By making extra payments, you can reduce your debt and save money on interest payments.

Communicate with Your Lender:

If you’re having trouble making your payments, it’s important to communicate with your lender. They may be able to offer you a repayment plan that suits your budget or help you find other options to manage your debt.

Ignoring your loan payments can lead to late fees and penalties and damage your credit score. If you’re struggling to make your payments, contact your lender as soon as possible to discuss your options.

Reduce Your Expenses:

If you’re finding it difficult to make your loan payments, consider reducing your expenses. This can help you free up some cash to put towards your loan repayment. Look for ways to cut back on unnecessary expenses, such as eating out less, canceling subscriptions you don’t use, or switching to a cheaper cell phone plan.

By reducing your expenses, you can free up some money to put towards your loan repayment.

Repaying your loan on time is essential for maintaining a good credit score and avoiding late fees and penalties. By following the tips above, you can create a solid repayment plan and ensure that you repay your loan on time.

Remember, borrowing money is a serious responsibility, and it’s important to take it seriously and manage your debt effectively. If you’re having trouble making your payments, don’t hesitate to contact your lender to discuss your options. With careful planning and discipline, you can manage your debt effectively and achieve your financial goals.

Spring into Savings: Tips for Maximizing Your Budget this Season.

Spring is a season of renewal, growth, and fresh beginnings. It’s also a time to reassess your financial goals and start taking steps to maximize your budget. With warmer weather and longer days ahead, it is the perfect time to make some changes to your financial habits and start saving money.

AAR Financial has some practical tips for springtime savings that you can start using today.

Set a Budget – Creating a budget can assist you in prioritizing your spending and identifying areas where you can save money. Start by making a list of all of your monthly expenses, such as bills, groceries, and entertainment. Then, compare your revenue to your expenses to identify where you may cut back. This can help you stay on budget and avoid overspending.

Spring Clean Your Finances – Just as you might deep clean your house in the spring, right now is a wonderful time to do the same with your finances. Examine your spending and identify places where you could potentially save money. Cancel any services you no longer use, renegotiate bills, and look for more cost-effective alternatives wherever possible. For example, if you’re not using your gym membership, consider canceling it and finding ways to exercise at home or outside.

Review Your Budget – The first step towards budget optimization is to examine your existing spending habits and find areas where you can reduce back. Analyze your monthly bills and spending to discover where you may save money. You may, for example, switch to a cheaper cell phone plan or negotiate a lower cable price. You can free up extra money to save or invest by making simple changes to your budget.

Save Money on Your Taxes – Spring is also tax season, and it’s important to take advantage of any tax breaks or deductions that are available to you. Make sure you’re claiming all of the deductions you’re entitled to, such as deductions for charitable contributions, medical expenses, and education expenses. You should also consider contributing to a tax-advantaged retirement account like an IRA or 401(k) to reduce your taxable income and save for the future.

Consider Refinancing Your Loans – With interest rates currently at a floating point, it may be a good time to refinance your loans in order to save money on interest payments. This is especially true if you have a credit card with a high-interest rate or a personal loan. You can cut your monthly payments and save money over the life of your loan by refinancing. If you have outstanding loans, now is an excellent moment to refinance, you may be able to save money on interest payments during the life of your loan. Refinancing may also lower your monthly payments, freeing up funds in your budget for other purposes.

Take Advantage of Seasonal Sales – Taking advantage of seasonal promotions is one of the simplest ways to save money in the spring. You’ll find lots of offers and discounts to take advantage of as businesses begin to clear out their winter inventory to make place for spring and summer merchandise. By keeping an eye out for specials and promos on everything from clothing to household products to gadgets, you can snag some fantastic deals.

To make the most of these deals, it’s important to plan ahead and know what you’re looking for. Create a shopping list of items you need or want to purchase and keep an eye out for sales and discounts on those specific items. You can also sign up for email newsletters or follow your favorite retailers on social media to stay up to date on their latest sales and promotions.

Finally, spring is an excellent time to reevaluate your financial habits and begin making changes to maximize your budget. You may save money and meet your financial objectives by examining your budget, taking advantage of seasonal specials, focusing on energy efficiency, and shopping wisely for food. So, start now and spring into savings!

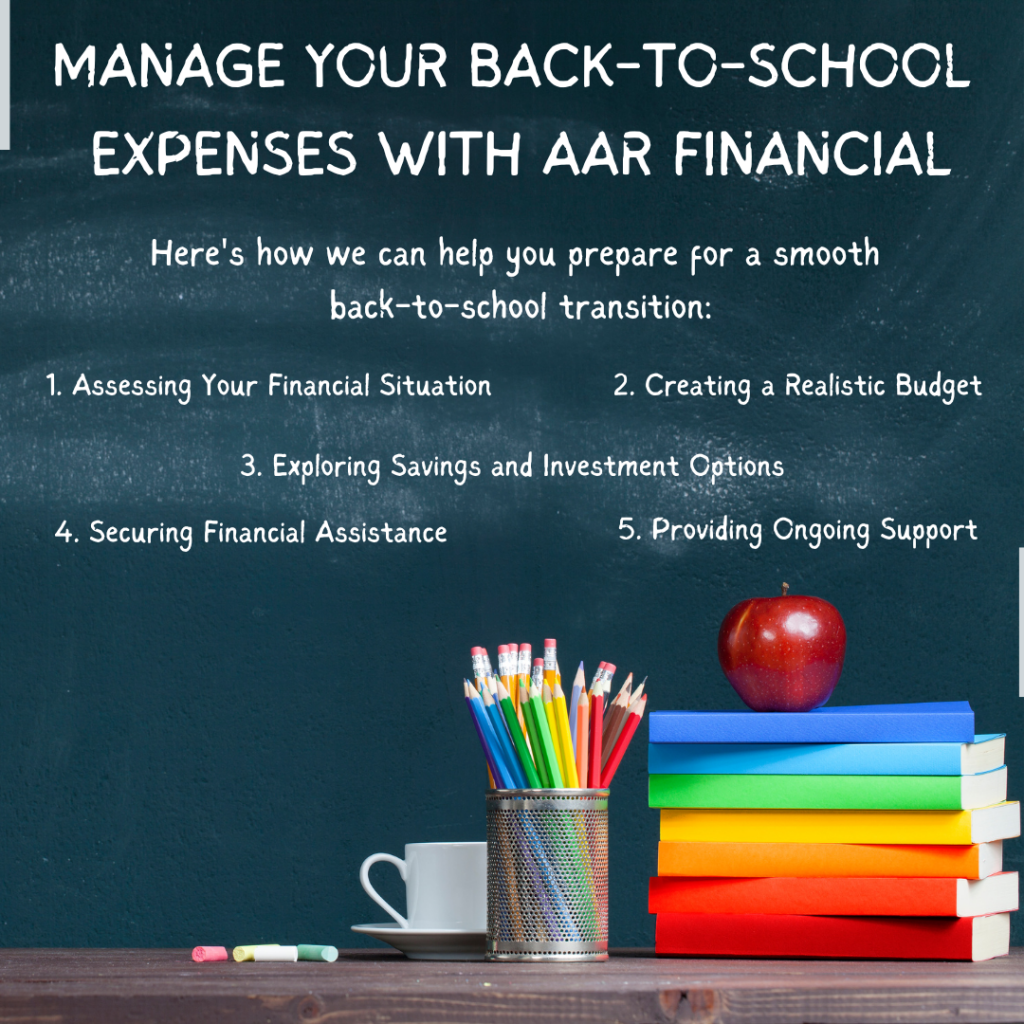

As the summer days start to wane, the excitement and anticipation of a new school year begin to build up.

For parents and students alike, this time of year is often met with mixed emotions—joy for the fresh start, but also concern about the impending back-to-school expenses. Thankfully, AAR FINANCIAL understand the importance of a smooth educational journey, and that’s why we offer hassle-free back-to-school loans to help you and your family make the most of this special time.

A Budgetary Challenge

The back-to-school season can be financially challenging for families, especially when considering the various expenses that need to be covered. From school supplies and uniforms to electronics and extracurricular activities, the costs can quickly add up, putting strain on your budget.

However, with careful planning and the right financial strategies, you can navigate this period with confidence. We believe that proactive financial planning is essential for managing back-to-school expenses without sacrificing your financial well-being.

At AAR FINANCIAL, we understand that each family’s financial situation is unique. Our team of expert advisors is dedicated to tailoring personalized financial plans that align with your specific needs and goals.

Here’s how we can help you prepare for a smooth back-to-school transition:

Assessing Your Financial Situation: Before diving into back-to-school shopping, it’s crucial to understand your current financial standing. Our financial advisors will work closely with you to review your income, expenses, savings, and any existing debts. With this comprehensive assessment, we can establish a clear picture of your financial capacity for back-to-school expenses.

Creating a Realistic Budget: Once we have a clear understanding of your financial situation, we’ll assist you in creating a realistic budget for the back-to-school season. This budget will encompass all necessary expenses, such as school supplies, uniforms, transportation, and extracurricular activities. By staying within your budget, you can avoid unnecessary financial stress and maintain control over your spending.

Exploring Savings and Investment Options: To help you better manage back-to-school expenses, our financial team will explore suitable savings and investment options. Whether it’s setting up a dedicated education savings account or exploring tax-efficient investment vehicles, we will ensure that you make the most of your hard-earned money.

Securing Financial Assistance: We understand that unexpected circumstances can arise, and financial assistance might be necessary. Our financial advisors can guide you through potential sources of aid, such as grants, scholarships, or low-interest loans, to ensure that you can access the support you need without compromising your financial stability.

Providing Ongoing Support: At AAR FINANCIAL, our commitment to your financial success extends beyond the back-to-school season. We offer ongoing financial guidance and support to help you stay on track with your financial goals throughout the school year and beyond.

As a leading financial institution, we take pride in our commitment to helping families achieve their educational goals. When you choose AAR FINANCIAL, you’re opting for a partner that understands the importance of education and aims to make it accessible to everyone. As the back-to-school season approaches, we stand ready to support you and your family in meeting all educational needs with our hassle-free Back-to-School Loans.

Reach out to AAR FINANCIAL today and let us be your partner in securing a successful and fulfilling academic journey for your child. Together, we’ll make the upcoming school year one of growth, knowledge, and accomplishment.

")

Navigating the Credit Maze: How to Get a Fall Loan with Less-Than-Perfect Credit

As the leaves begin to change and the air becomes crisp, the fall season brings with it a sense of renewal and change. It’s a time for cozy sweaters, pumpkin spice lattes, and planning for the holidays. For many, this season also comes with financial considerations. Perhaps you’re looking to fund a home renovation project, take a dream vacation, or cover unexpected expenses. But what if you have less-than-perfect credit?

Can you still secure a fall loan to make your autumn dreams a reality? The answer is yes, and in this article, we’ll show you how to navigate the credit maze and obtain a fall loan, all while working towards improving your credit score.

Understanding the Importance of Credit Score: Credit scores play a crucial role in our financial lives, especially when it comes to obtaining loans. Lenders rely on credit scores to assess the level of risk associated with lending money to individuals. Your credit score reflects your creditworthiness and indicates how likely you are to repay borrowed funds. It is based on factors such as your payment history, credit utilization, length of credit history, types of credit used, and recent credit inquiries.

Explore Your Loan Options: Before you embark on your journey to secure a fall loan, it’s crucial to know where you stand. Obtain a copy of your credit report and review your credit score. Understanding your current credit situation will help you make informed decisions. The lending landscape is diverse, and there are various loan options available, even if you have less-than-perfect credit. These may include:

Personal Loans: These unsecured loans can be used for various purposes, making them a flexible option.

Secured Loans: Secured loans are backed by collateral, such as a car or savings account. Lenders may be more willing to approve a loan when there’s collateral involved.

Peer-to-Peer Lending: Online platforms connect borrowers with individual investors who may be more open to lending to those with imperfect credit.

Building a Strong Loan Application: To increase your chances of approval, create a compelling loan application. This includes showcasing your strengths:

– Highlight your steady income and employment stability.

– Offer collateral, if possible, which can give lenders added security.

– Provide a clear plan for how you will use the loan funds and how you will make repayments

Consider a Co-Signer: Collateral refers to assets that you offer to the lender as a guarantee that you will repay the loan If your credit score is significantly low, consider enlisting the help of a co-signer with good credit. This person’s creditworthiness can boost your application’s appeal to lenders.

Presenting strong collateral can greatly improve your chances of approval. By offering valuable collateral, you demonstrate to the lender that you have something of value to lose if you default on the loan. This reduces their risk and makes them more likely to approve your loan application.

Preparing Yourself for the Responsibilities of Borrowing Money: Work on reducing existing debts. Lowering your debt-to-income ratio can make you a more attractive candidate for lenders. It’s important to prepare yourself for the responsibilities that come with borrowing money. While a loan can provide the financial boost you need, it’s crucial to approach borrowing with caution and a clear understanding of your obligations.

First and foremost, make sure you fully comprehend the terms and conditions of the loan before signing any agreement. This includes understanding the interest rate, repayment schedule, and any associated fees. It’s also important to carefully consider your budget and ensure that you can comfortably make the monthly payments without straining your finances.

Additionally, it’s crucial to prioritize loan repayment and make timely payments. Missing or delaying payments can result in late fees, damage to your credit score, and even potential legal action from the lender. Set up reminders or automatic payments to stay on top of your obligations and avoid any unnecessary complications.

As you work on securing a fall loan, regularly monitor your credit report. As your financial habits improve and your credit score increases, you may become eligible for better loan terms and lower interest rates.

Finally, securing a fall loan with less-than-perfect credit may require extra effort and careful planning, but it’s entirely achievable. By following these steps and making responsible financial decisions, you can not only obtain the funds you need for your autumn plans but also take significant steps toward improving your credit score.

Fall is a season of change and renewal, and with the right strategies, you can navigate the credit maze and emerge with a stronger financial standing, ready to enjoy the beauty and opportunities the season brings.

“ Remember, borrowing is a financial commitment, so it’s crucial to approach it with responsibility and awareness” – AAR Financial !

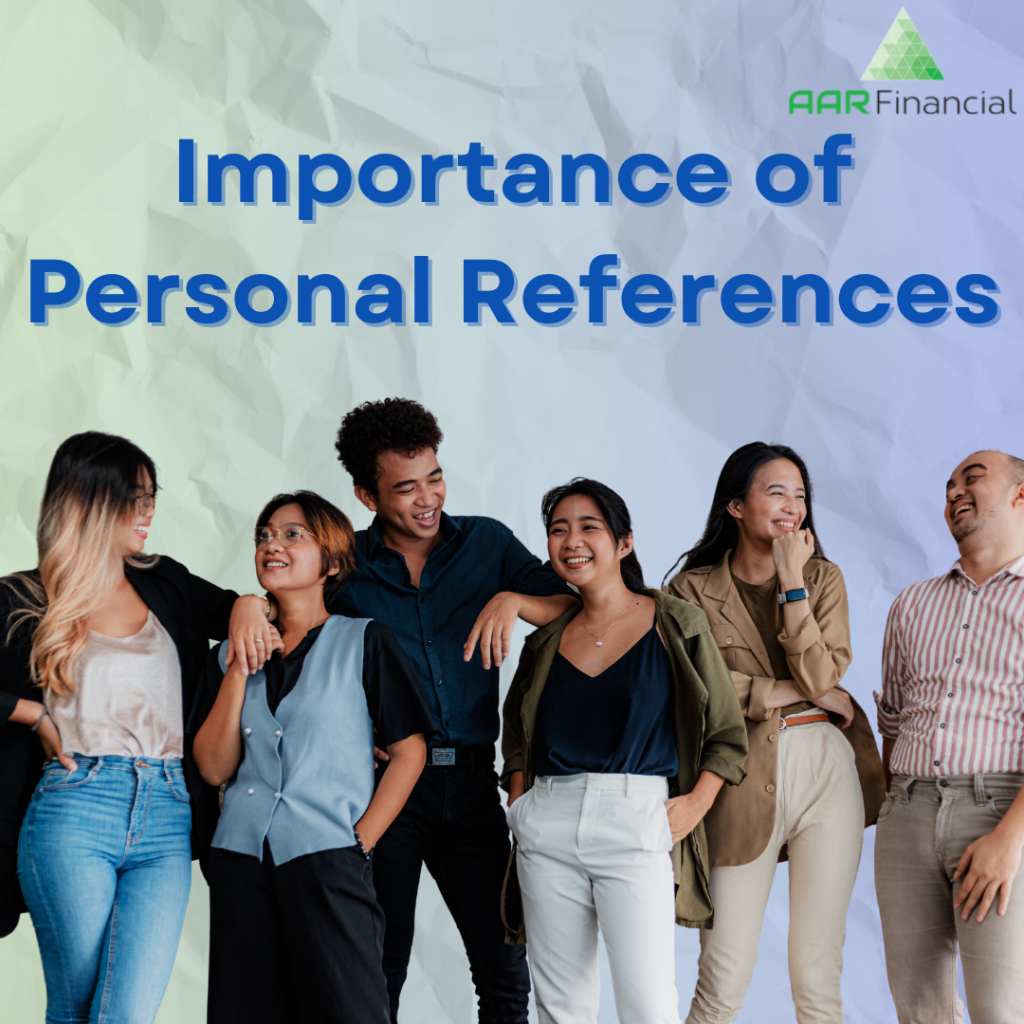

Role of Personal References in Your Loan Application

If you’ve ever ventured into the world of loan applications, you’ve probably raised an eyebrow at the mention of personal references. It’s a common practice among lenders, and on the surface, it may seem unnecessary. However, there’s more to this than meets the eye.

In this blog post, AAR Financial will embark on a journey to uncover the ‘why’ and ‘how’ of personal references in the loan application process. By the end of this exploration, you’ll not only understand their importance but also discover the mutual benefits they offer to both borrowers and lenders. Armed with this knowledge, you’ll be better prepared to navigate the loan application process with confidence. So, let’s delve into the intriguing world of personal references and see how they play a crucial role in the lending landscape.

- Verifying Identity

One of the primary reasons lenders ask for personal references is to verify your identity and character. By contacting your personal references, lenders can confirm that the information you provided in your loan application is accurate. They may ask about your relationship, how long you’ve known each other, and your general character traits. This verification process helps lenders assess your credibility and determine your likelihood of repaying the loan.

- Building Trust and Credibility

Lenders place great importance on trust and credibility. When you willingly provide personal references, you signal your commitment to transparency and candor concerning your financial history. This, in turn, fosters a foundation of trust between you and the lender, bolstering their confidence in your application. Lenders are driven by the desire to establish you as a reliable borrower, secure in the knowledge that the information you furnish can be counted upon.

- Evaluating Character and Responsibility

Personal references can shed light on your character and sense of responsibility. Lenders want to ensure that borrowers are financially responsible and will repay their loans as agreed. Positive references from individuals who can vouch for your integrity and reliability can significantly impact the lender’s decision in your favor.

- Assessing Stability

Furthermore, lenders utilize personal references to assess your financial stability comprehensively. In these conversations, they might delve into your employment track record, the consistency of your income, and your overall financial accountability. This includes your capacity to manage financial obligations and adhere to punctual payment schedules.

- Addressing Limited Credit History

For individuals with limited credit history, personal references can be especially valuable. References can help compensate for a lack of established credit by providing alternative evidence of your trustworthiness and financial responsibility.

- Reducing Risk for Both Parties

Lending involves a certain degree of risk for both borrowers and lenders. Personal references help reduce this risk by giving the lender a broader perspective on your financial situation. This, in turn, can lead to more favorable loan terms for borrowers. In case of unforeseen circumstances or difficulties in contacting you, lenders can reach out to your personal references for assistance.

- Proving Repayment Capacity

Your personal references may be asked about your financial habits, including your ability to repay loans. Their statements can support your case, especially if you have a stable income and a history of responsible financial behavior.

- Compliance with Regulations

In some cases, regulatory requirements or internal policies may mandate the collection of personal references as part of the loan approval process. Compliance is crucial for lenders to avoid legal issues and maintain a trustworthy reputation.

- Demonstrating Commitment

By providing personal references, you signal your commitment to the loan application process. Lenders appreciate borrowers who are willing to cooperate and provide the necessary documentation, as it reflects positively on their seriousness about the loan.

Tips for Providing Personal References:

- Choose Reliable and Trustworthy References: Select individuals who know you well, such as close friends, family members, or colleagues who can vouch for your character and financial responsibility.

- Notify Your References: Inform your personal references in advance that they may receive a call from your lender. This ensures they are prepared and can provide accurate information.

- Maintain Open Communication: Stay in touch with your personal references throughout the loan application process. Keep them informed about the progress and provide any updates if necessary.

At AAR Financial, we understand the significance of personal references and aim to make the lending process as transparent and efficient as possible. If you have any questions or concerns about the use of personal references in our loan approval process, please feel free to reach out to our team. We’re here to help you achieve your financial goals.

")

Financially Savvy Holidays – A Guide to Smart Planning

The holiday season is a time of joy, celebration, and giving which is just around the corner, and it’s the perfect time to start planning for the festivities. Whether it’s decking the halls, preparing lavish feasts, or exchanging gifts with loved ones, the holidays bring joy and warmth to our lives. However, amidst the merriment, it’s essential to ensure that our financial well-being remains intact. As we gear up for the holiday season, it’s crucial to strike a balance between celebrating and managing our finances wisely.

At AAR Financial, we understand the significance of financial preparedness during the holiday season. As a trusted provider of personal and mortgage loans, we are committed to helping individuals navigate their financial obligations while embracing the spirit of the holidays. In this comprehensive blog post, we’ll delve into practical tips on how to prepare for the holidays while also shedding light on how our financial services can support you during this festive season.

Budgeting for Festive Celebrations:

Embarking on a successful holiday season begins with the crucial step of setting up a realistic budget. This initial measure involves outlining anticipated expenses for gifts, decorations, travel, and entertainment. By doing so, you can gain a comprehensive understanding of your financial commitments and ensure that your holiday celebrations align with your financial capabilities. We will delve into valuable insights on crafting a holiday budget tailored to your needs, empowering you to partake in the festivities without encountering undue financial strain. Remember, starting with a clear budget is the key to preventing overspending and maintaining financial balance during the holiday season.

Take Advantage of Deals and Discounts:

Discuss and establish gift-giving expectations with friends and family. Consider alternatives like Secret Santa or setting spending limits to make the season more affordable for everyone. Remember, the value of a gift is in the thought and effort, not necessarily the price tag.

Keep an eye out for holiday sales, discounts, and promotions. Many retailers offer special deals during the holiday season. Take advantage of these opportunities to save money on gifts and other purchases.

Use Cash or Debit Cards:

As the holiday season approaches, the allure of resorting to credit cards or loans to finance festivities can be compelling, we will offer valuable guidance on the responsible utilization of credit and loans, underscoring the significance of mindful borrowing and judicious financial decision-making.

Opting for cash or debit cards for your holiday expenditures, as opposed to relying on credit cards, is a prudent approach. This not only aids in adhering to your budget but also helps steer clear of accruing avoidable debt. In the event that credit cards are utilized, it’s imperative to promptly settle the balances, ensuring a responsible and manageable financial approach during the holiday season.

Review Your Financial Goals:

Take some time to review your financial goals for the upcoming year. This might include saving for a vacation, creating an emergency fund, or contributing more to your retirement accounts. Setting financial resolutions can help you start the new year with a clear financial vision.

Set aside a portion of your income throughout the year specifically for holiday expenses. Creating a separate savings fund for the holidays can alleviate financial stress and provide a financial cushion when needed.

Showcasing Our Financial Services

As a reputable provider of personal and mortgage loans, we will spotlight how our financial services can support individuals during the holiday season. From flexible loan options to personalized financial solutions, readers will gain valuable insights into how our offerings can alleviate financial stress and enhance their holiday experience.

By combining practical holiday preparation tips with a focus on financial well-being, our blog aims to empower readers to embrace the holiday season with confidence and financial mindfulness. At AAR Financial, we are dedicated to fostering financial resilience and enabling individuals to celebrate the holidays without compromising their financial stability.

As the holiday season approaches, let’s embark on a journey of festive joy while upholding financial prudence. Stay tuned as we unveil a wealth of insights and guidance to make this holiday season a harmonious blend of celebration and financial preparedness.

By incorporating these financial tips into your holiday planning, you can enjoy a season filled with joy and festivities without compromising your financial well-being. Remember, smart financial decisions during the holidays can set the tone for a prosperous and financially healthy new year. Cheers to a happy and financially savvy holiday season!

99

%

Approval Rate

10000

+

Happy Customers

100

%

Transparent Process

Frequently Asked Questions?

- We are a private lending institution based out of Winnipeg, Manitoba and we serve all surrounding regions. At AAR Financial, we offer personal loans up to $50,000 and home equity loans up to $100,000 in Manitoba, Saskatchewan, Alberta, Ontario & BC.

- By getting a loan from AAR Financial, we can pay off your other creditors or accounts with other companies and you will have just one manageable payment with us.

- Although your credit score is a factor in our decision, many other factors play into our decision of whether to advance cash to you. Having excellent credit is not a pre-requisite. Apply now and see how much you qualify for!

QUICK LINKS

CONTACT US

823 Regent Avenue West, Winnipeg Manitoba. R2C 3A7

Call Today – (204) 224 3271

Email us- info@aarfinancial.ca

Visit us in store!

– Loan terms range from 2 years to 10 years APR: 14.9% – 46.7% Financial Example – $1,000 borrowed for 12 months at 46.67% APR. Biweekly payment = $ 48.47, total repayment with Interest is $1,260.22. Total Cost of the loan = $ 260.22. Finance Example includes optional loan protection coverage. For more detail, please contact us at (204) 224- 3271.

– License Number #84231 (BC) , #349447 (AB)

– Copyright © 2022 AAR Financial Incorporated all rights reserved.